Market Highlights

- Geopolitical tensions have intensified with Iran’s attack on Israel.

- Coinbase will delist USDT and other stablecoins in the EU by year’s end.

- The Howey Test may be put to the test in the Ripple and Coinbase cases, each being heard before the same US district court.

- The filmmaker of an HBO documentary says the film will reveal the identity of pseudonymous Bitcoin creator Satoshi Nakamoto.

In Case You Missed It

Inside the Markets with Caleb & Brown | October 2024

In our first episode of Inside the Markets, our Chief Commercial Officer, Jake Boyle dives into; September’s crypto and macro highlights—covering U.S. Fed rate cuts 🏦, China’s stimulus 🇨🇳, and key geopolitical events 🌍.

Looking ahead, we explore Bitcoin's historical Uptober trend, the impact of upcoming U.S. elections, and FTX claim distribution.

➡️ Watch Now!

Markets Overview

Macro Market Updates:

A stronger-than-expected employment market update from the US followed by Federal Reserve Governor Jerome Powell’s statement at a conference hosted by the National Association for Business Economics, reignited macro uncertainty this week. In his statement, Powell said the central bank’s “base case” is to deliver two small rate cuts before year’s end. The US non-farm employment change for September came in at 254,000, much higher than the forecast of 147,000. Similarly, the unemployment rate came in just under forecast at 4.1%.

Also this week, geopolitical tensions rose as Iran launched 200 ballistic missiles towards Israel on Tuesday, 1 October. Most of the missiles were intercepted by the Israeli military. This attack follows Iran’s April attack, where it launched 300 missiles and drones. Though markets haven’t seen a significant sell-off, Iran’s second attack on Israel, plus the ongoing warfare in Ukraine that is currently over 950 days long, indicate that ongoing geopolitical risk could impact risk-on assets, such as crypto and equities.

Other macro data releases this week included consumer price index (CPI) and purchasing manager index (PMI) updates:

- The US ISM manufacturing PMI came in at 47.2.

- US unemployment claims came in just over forecast at 225,000.

- Inflation in Switzerland fell to a three-year low of -0.3% in September 2024.

Crypto Market Sector Performance

Sector growth was mixed this week. Artificial intelligence (AI), social networks and file storage led the way led the way.

The growth seen in AI this week is presumably due to an uptick in investor interest in AI-driven networks and applications. Synesis One (SNS) and Zero1 Labs (DEAI) were some of the biggest AI and big data gainers for the week, growing by 34.8% and 32.4%, respectively. SNS has seen a bull run of over 300% since late September, likely due to its new strategic partnership with decentralised data storage network Stratos and a collection of positive updates in its Q3 newsletter. Similarly, Zero1 Labs announced positive developments in its September monthly update last week, including a new centralised exchange listing and the announcement of deflationary measures to buoy the price of $DEAI and combat devaluation through inflation.

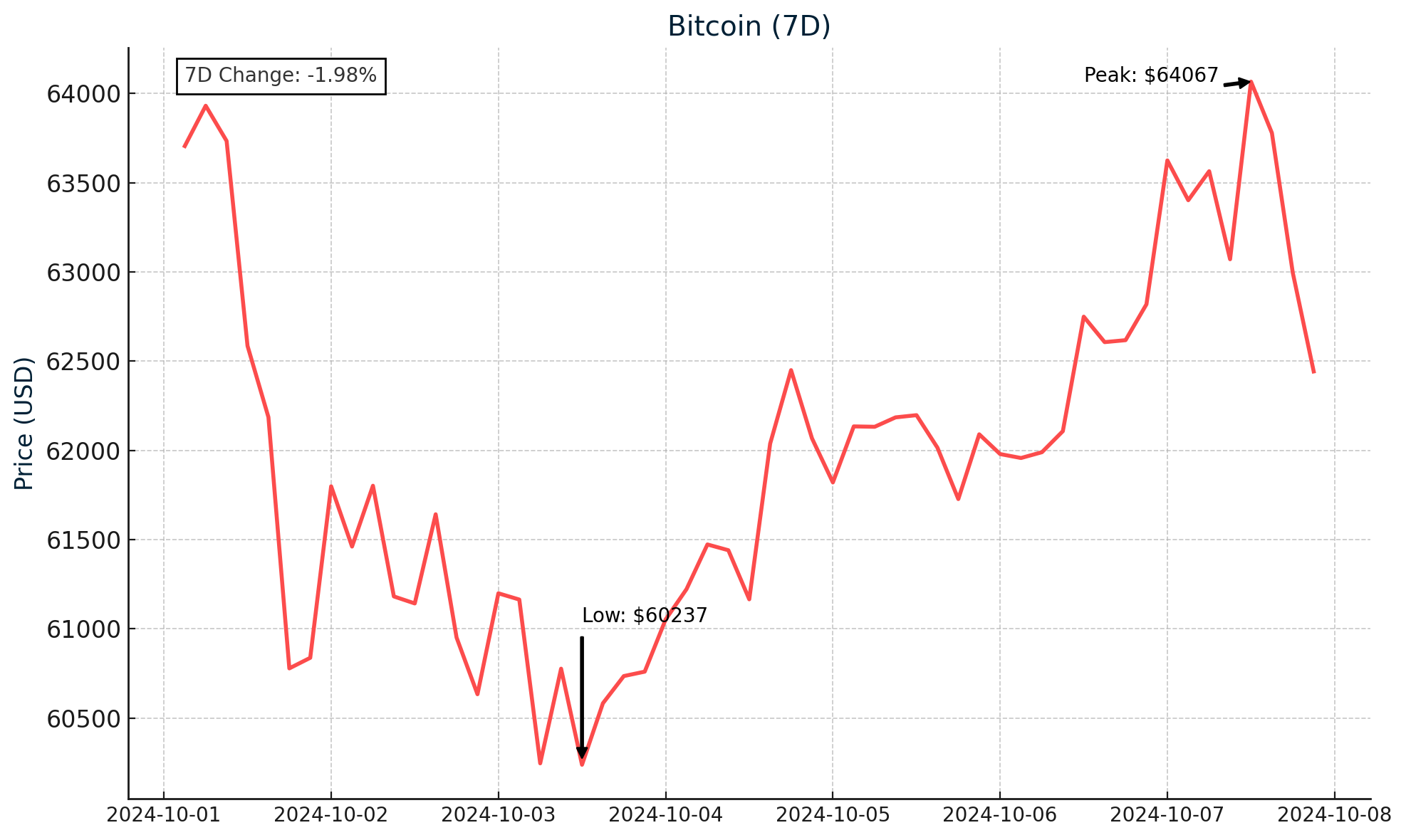

Bitcoin (BTC)

It was a relatively quiet week for bitcoin, with small losses occurring. Opening the week at US$65,759, price declined over 8% to a low of US$60,004 on Thursday before recouping some of the week’s losses.

The sell-off to start the week is presumably due to geopolitical tension in the Middle East, the strong US jobs report that signalled smaller rate cuts may be the US Federal Reserve’s agenda for the remainder of 2024, and another whale moving their bitcoin to a centralised exchange. The “ancient” bitcoin whale hadn’t transacted since they first mined some bitcoin one month after the cryptocurrency was created. Almost US$3.6 million worth of bitcoin was moved to crypto exchange, Kraken. The whale still has over 1,1189 bitcoins worth nearly US$77 million, but any movement of bitcoin to a centralised exchange can signal the potential for a whale to sell, which can cause market jitters.

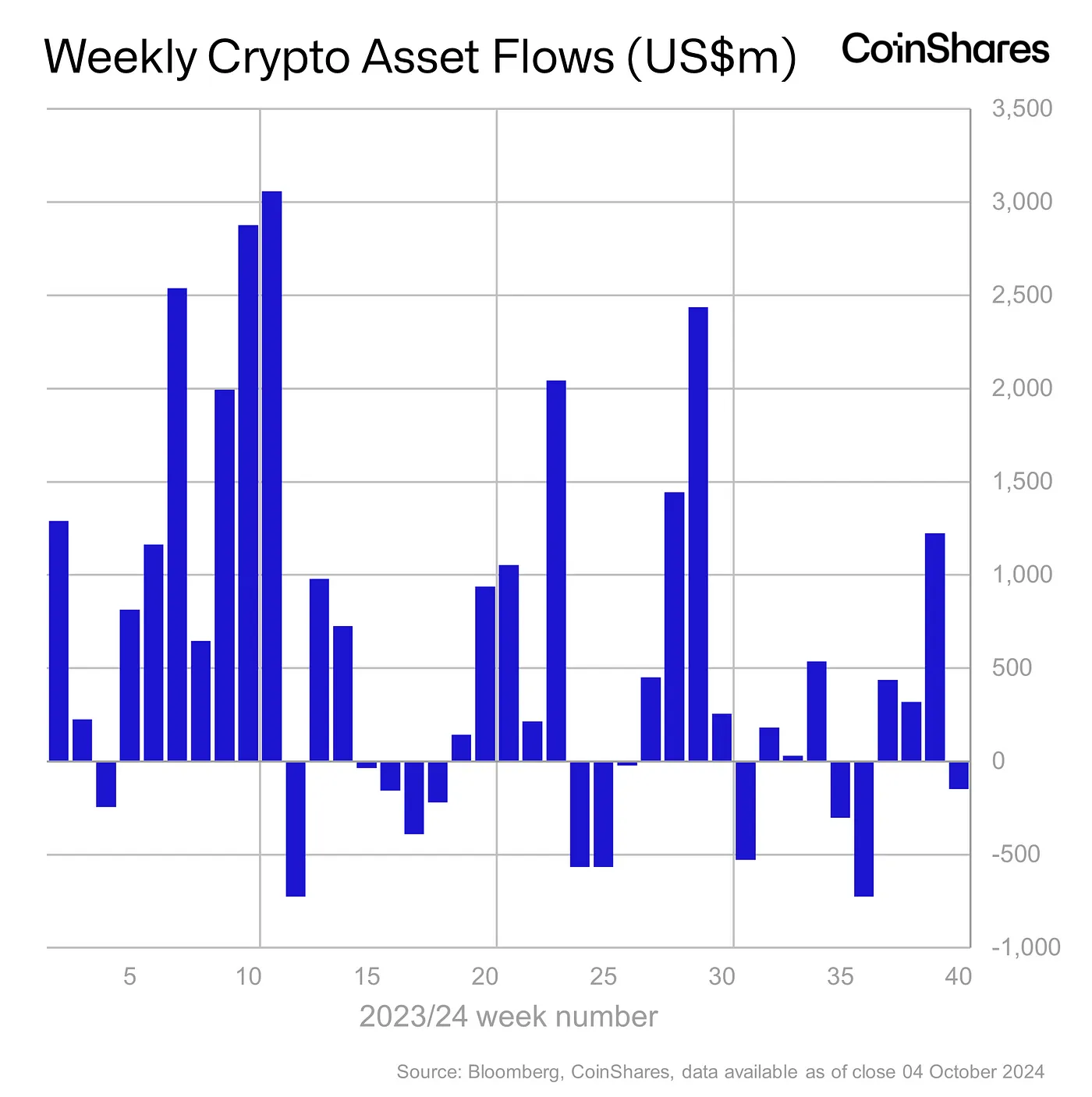

It was a big week of outflows for bitcoin asset investment products, with outflows totalling US$147 million. Short-bitcoin products saw inflows of US$2.8 million.

A documentary released on Tuesday, 9 October, will purportedly reveal the identity of Bitcoin’s creator, Satoshi Nakamoto. Money Electric: The Bitcoin Mystery will dive into the question of who invented Bitcoin and whether it was one person or a group of people. It’s rumoured that American cypherpunk and cryptographer Leonard Harris “Len” Sassaman may be revealed as the inventor of Bitcoin. Sassaman died in 2011.

Japanese investment firm Metaplanet acquired a further 107.9 bitcoin for approximately US$6.6 million this week. This takes the firm’s bitcoin holdings to 506.7, worth about US$31.8 million. Their average purchase price is US$62,712 per bitcoin. With this latest purchase, Metaplanet’s bitcoin holdings are now worth almost 20% of the firm’s US$125 million market capitalisation. Mirroring US software company MicroStrategy’s (MSTR) approach, Metaplanet dubbed itself “Asia’s first MicroStrategy” when the company announced its bitcoin treasury strategy in April 2024. Metaplanet’s stock price has gained over 450% since April.

Ethereum (ETH)

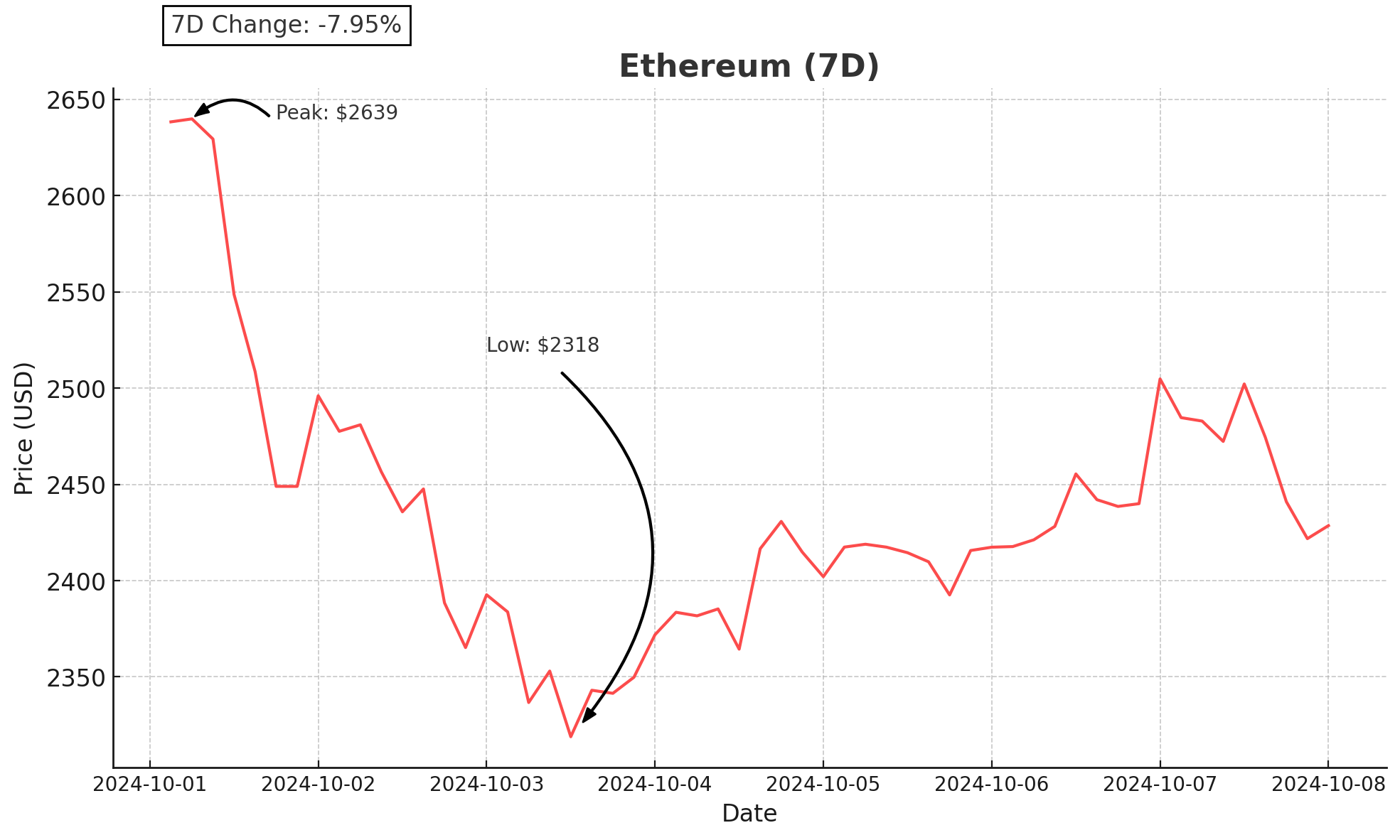

Ethereum’s price action saw a sell-off followed by a bounce off key support at US$2,320 to end the week with losses of just over 6%. The second biggest cryptocurrency by market cap opened the week at US$2,655, sold off to the key level at US$2,320 and regained strength with a rebound of almost 7%.

Outflows continued for Ethereum asset investment products this week, with US$29 million leaving funds. The total assets under management for these products currently stands at US$9.8 billion.

Vitalik Buterin, co-founder of Ethereum, published a blog post this week outlining what he believes could be the metrics to assess “Ethereum alignment”. Given the network’s decentralised nature, Buterin said, "A key goal of Ethereum alignment is making sure that the protocol is a ‘credible neutral platform’.” Key areas where Buterin thinks different stakeholders should be aligned include adherence to protocol upgrades, engagement in governance, and efforts to minimise centralisation risks.

Ethereum’s volatility readings are currently larger than bitcoin’s, with forward volatility between October 25 and November 8 coming in at 76.6% and 69.8%, respectively. The difference in volatility between the two largest cryptocurrencies has widened in recent months due to macro uncertainty, especially the upcoming US presidential election. At the time of writing, the gap in implied volatility for 30-day at-the-money Ethereum contracts has grown to 7%. The widening gap indicates that traders are getting positioned for volatility in the coming weeks. Ethereum’s higher implied volatility suggests it may be more heavily impacted by events that cause a spike in volatility.

Altcoins

Who are you?

- Civic (CVC) gained 71.1%, taking its market cap to US$170.6 million. Price for the web3 identification and age verification platform took off on Friday, 4 October when price found support around the convergence of the 200-day and 50-day moving averages. This strong technical price action, plus the network’s continued engagement efforts around Civic Pass, its identification technology that has multiple applications, have peaked further investor interest, which has presumably driven this most recent bull run.

Multiple (data) sources

- DIA (DIA) gained 62.8%. This takes its market cap to US$89.5 million. In another strong week for the trustless Oracle network, price gained almost 140% before retracing slightly. This week’s run is presumably due to the integration of crypto exchange BitGet as a data source, allowing DIA to generate price oracles for any token traded on the platform. It follows a string of new partnerships and an integration with Stacks, which were all announced in September.

DeFi gains and listings

- Mdex (HECO) gained 38.8%, taking its market cap to US$20.6 million. The gains from the automated market maker (AMM) are presumably due to continued investor interest in networks that integrate and aggregate an array of data and services in one location.

- Reef (REEF) increased by 30.7%. This takes the DeFi network’s market cap to US$154.9 million. The layer-1 blockchain that provides DeFi, NFTs and gaming functionality has seen strong gains since August. The most recent gains are presumably due to gTrade, an on-chain leverage trading network, listing REEF on its platform.

In Other News

Digital asset investment products saw outflows of US$147 million this week. The outflows were presumably driven by weakening macro sentiment. The US saw the largest outflows, with US$209 million leaving funds. Hong Kong and Germany followed, with outflows of US$8.3 million and US$7.3 million, respectively. The outlier this week was multi-coin investment products. Marking their 16th consecutive week of inflows, US$29 million flowed into these funds.

- Investment firm Grayscale has launched a fund that gives accredited investors exposure to Aave (AAVE). As the 44th largest cryptocurrency by market cap, Aave has seen gains of almost 100% since August before retracing back to the 50-day moving average and finding support in this zone in recent weeks. The fund will be closed-end, meaning it will not operate like an exchange-traded fund (ETF), which is typically more liquid as investors can buy and sell assets at almost any time.

- Franklin Templeton has expanded its listed on-chain US Government Money Fund (FOBXX) to the Aptos blockchain. Aptos is a decentralised network created by some of the team who created Meta’s now-defunct Diem project. As the first and only US-registered fund where transactions are stored on a public blockchain, investors can buy shares of FOBXX to gain exposure to US Government securities, cash and repurchase agreements.

Regulatory

- Coinbase announced that it’s going to delist some of its stablecoins, including USDT, Tether’s US dollar-pegged stablecoin. The move from the crypto exchange comes as a result of regulatory pressure from the European Union’s Markets in Crypto Assets (MiCA) regulation. This piece of regulation provides guidelines for crypto assets that don’t currently fall under the jurisdiction of existing EU legislation. Under MiCA, algorithmic stablecoins will be banned in the EU. USDT will be delisted from Coinbase by 30 December 2024.

- The US Securities and Exchange Commission (SEC) has appealed a court ruling in the Ripple case, arguing that it conflicts with established Supreme Court precedent regarding securities definitions. The SEC contends that the United States Court of Appeals for the Second Circuit misapplied the Howey test, which determines whether an asset qualifies as a security. On August 7, a judge ordered Ripple to pay a civil penalty of US$125 million, much lower than the SEC’s requested US$2 billion penalty.

- Following the SEC’s appeal on the Ripple case, Coinbase has asked the judge hearing the company’s case to grant an interlocutory appeal (an appeal approved before the case is decided). This follows Coinbase’s original filing for an interlocutory appeal in early April. A letter from the company states that having Coinbase’s appeal presented to the United States Court of Appeals for the Second Circuit at the same time that the SEC’s appeal in the Ripple case is presented will provide a “…full account of the legal and practical implications of the SEC’s litigating position.”

from Caleb & Brown Cryptocurrency Brokerage.