Overview

- Celsius, the largest centralised crypto lending platform, has become functionally insolvent following a crypto “bank run”.

- Subsequently, the platform has suspended all withdrawals, swaps, and transfers pointing to ‘extreme market conditions’ as the reason for the freeze leaving deposit holders without liquidity.

- Celsius’ governance token CEL rapidly lost ~60% between the 7th and 13th of May 2022, recovering post the ongoing withdrawal freeze.

- This comes as Celsius struggled to liquidate approx. US$500m of stETH holdings, an illiquid asset that the platform used to generate interest on Ethereum (ETH), as crypto market volatility decimated the platform’s current liquidity.

- Investment Bank Goldman Sachs are looking to raise US$2b to purchase Celsius’ assets if they do become bankrupt.

- This is the second major crypto business or project collapse in recent months. While the estimated dollar value of this collapse is comparable to that of Lehman Brothers during the Global Financial Crisis (GFC) of 2008, no government bailout is on the horizon for Celsius.

- Caleb & Brown does not engage in DeFi lending or staking and retains all client assets with immediate availability for the client. We remain the vanguard of the cryptocurrency industry, exercising expertise in prudential capital management in digital asset and cash holdings on a conservative basis, whilst carrying no debt to any third party.

What is Celsius?

Celsius is a centralised finance (CeFi) cryptocurrency lending platform, which offers a variety of fintech services within the crypto space. The primary offering is interest-generation on assets such as Ethereum (ETH) for deposits made to their platform, as well as crypto-collateralised loans, trading services for major coins and cryptocurrency funds management services.

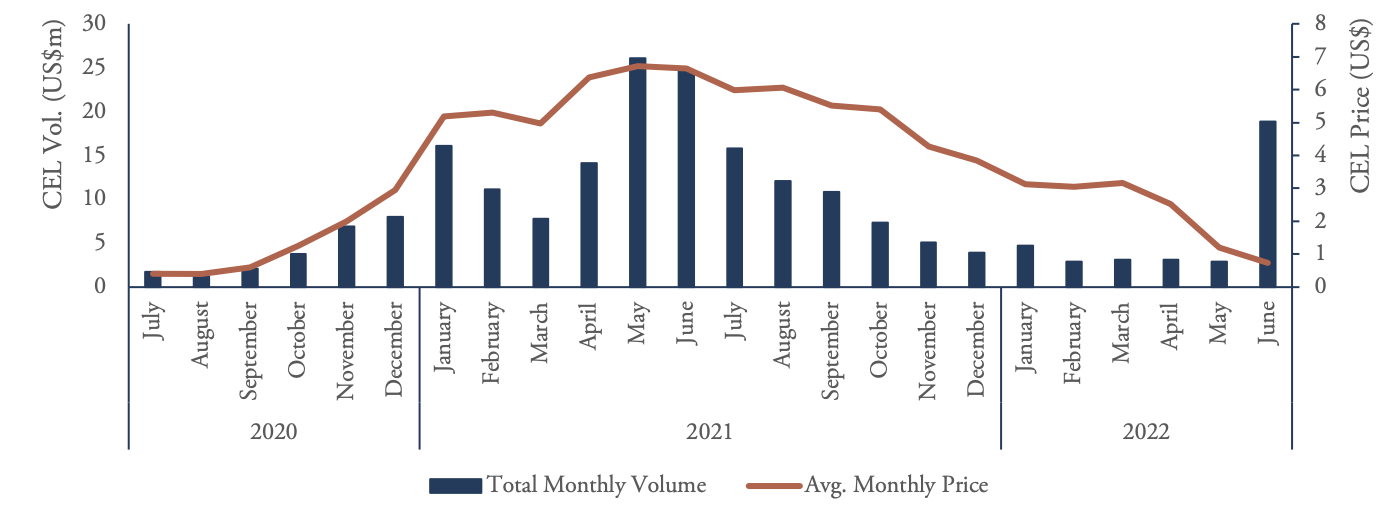

Celsius flourished throughout the 2020/21 bull market securing a US$750m series B funding round in late 2021 (valuingCelsius at US$10b). As of October 2021, Celsius held around US$25b worth of deposits (nearly 1% of the total crypto market capitalisation at the time). However, in line with the cryptocurrency market drop of over 70%, Celsius’ holdings have declined to US$11.8b of deposits on May 17th, further causing the traded value of CEL to fall, as indicated in the chart below.

How Does Celsius Work?

Celsius reinvests deposited funds to the platform in other crypto-derivative products which generate a return that is then partly paid to deposit holders and retained by Celsius. In this way Celsius functions in a similar way to a traditional bank through balancing the short-term liquidity needs of the client and the long-term loans issued, as well as other interest generation positions taken.

Celsius also issue the token $CEL which is used to attract users to the platform by offering discounted loan fees, and greater yields on deposits if paid out in $CEL.

For traditional and regulated banks, functioning in this way is not an issue as there is a greater level of regulatory oversight allowing for daily liquidity to be effectively managed, although traditional banks do not issue their own currency.

However, Celsius is inherently exposed to cryptocurrency volatility in which periods of severe market swings result in large demand for withdrawals from users, straining the platform’s short-term liquidity to meet unpredictable demand.

Celsius Withdrawal Problems

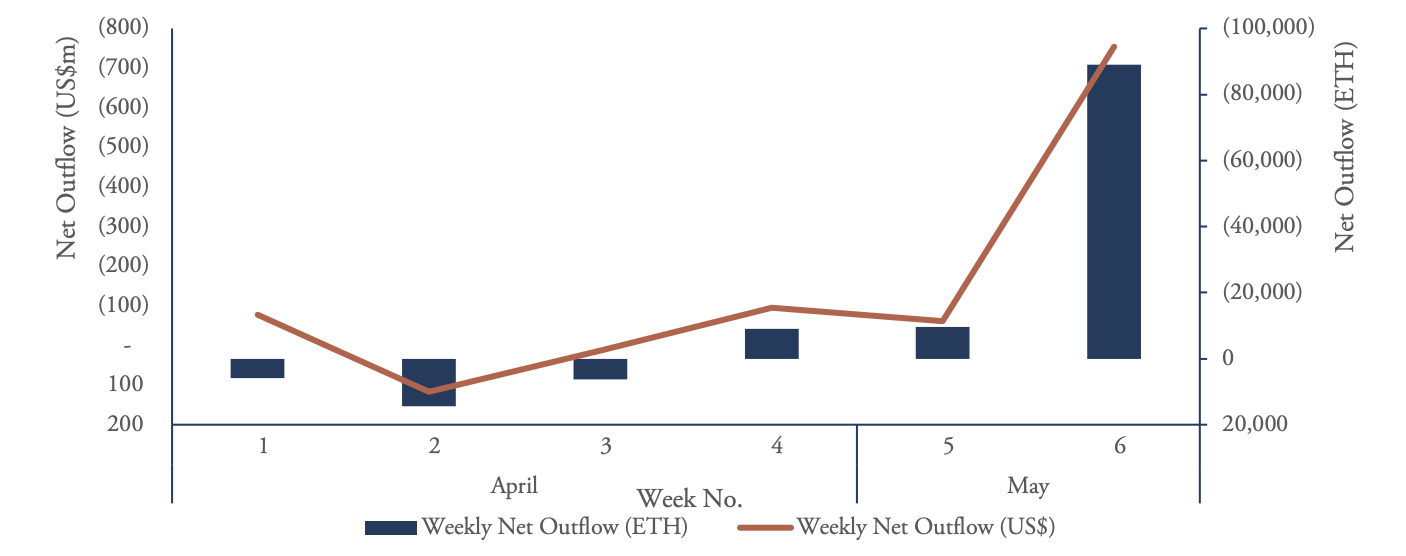

Recent market volatility and the Terra (LUNA) collapse resulted in a spike of Celsius clients requesting withdrawal of their deposits on demand (chart below), as rumours emerged that the platform was exposed to an imbalance between short-term liquidity and its long-term lending/yield generation positions currently at risk in the market.

These yield generation positions (i.e., staking contracts) have pre-defined contract lock-up dates which must vest for the cryptocurrency asset to be redeemable and sold on market or withdrawn by Celsius’ clients, thereby providing liquidity.

The chart below indicates that the withdrawal concerns first spiked in April 2022, following the negative and bearish macroeconomic environment building because of high U.S. inflation and the interest rate environment.

As a result, more assets were leaving the Celsius platform on a weekly basis, exposing the shortfall in the liquid current capital assets held by Celsius to settle immediate callable deposits held by clients, peaking to US$754m in net assets removed between the 6th and 12th of May 2022.

Celsius previously posted net deposit and withdrawal positions on a weekly basis on Twitter, however, has not posted since May 13th indicating that the platform’s balance sheet is unhealthy and likely to be insolvent.

Celsius’ Exposure to ETH & ETH2

Ethereum 2.0 (ETH2) is an upgrade to the Ethereum blockchain aimed to increase the scalability, decentralisation and security of the network so that it can avoid bottlenecks and mitigate concerns around the ‘Blockchain Trilemma’.

The Ethereum upgrade (“the Merge”) is the most significant upgrade undertaken for the network and greatly anticipated as crypto market participants, as it will completely reshape how Ethereum functions going forward. It aims to mitigate the network’s weak-points by changing the consensus mechanism from proof-of-work (PoW) to proof-of-stake (PoS).

Celsius allocated nearly half of all ETH holdings to ETH2 through liquid staking, representing a significant exposure and a long-term play on the success of the late 2022 forecasted Ethereum network upgrade.

Celsius, Liquid Staking, ETH2 & stETH

Liquid staking is the method with which Celsius generates yields on deposits. Celsius removed deposits from ETH holdings to pooled third-party staking services such as Lido, which issues the liquid staking token stETH (i.e., stakedETH).

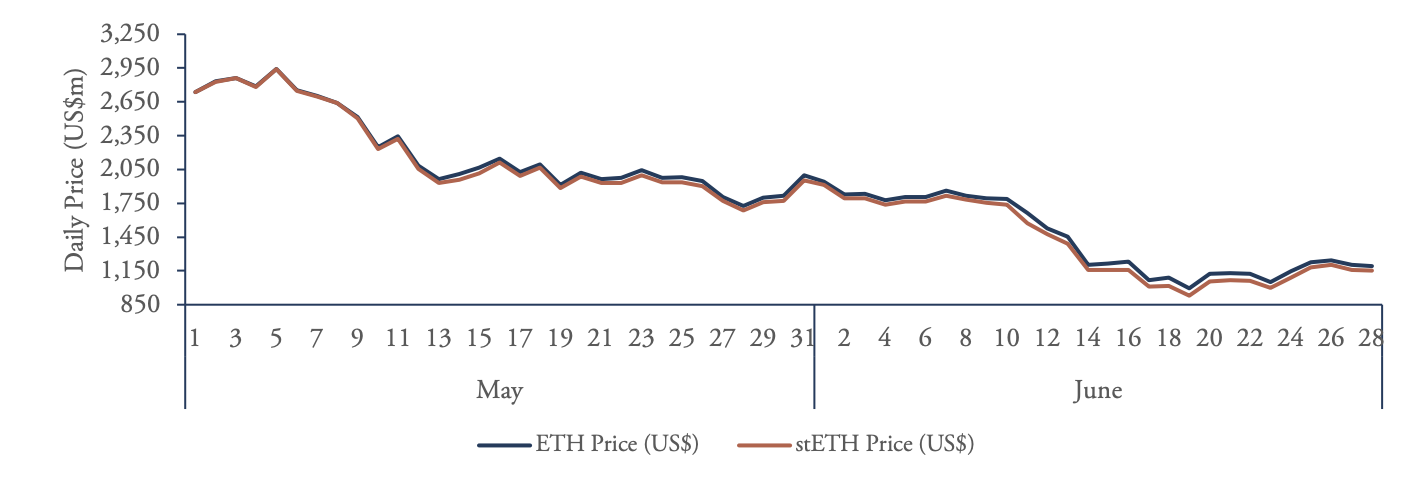

In this way, 1 ETH is exchanged by Celsius for 1 stETH, but this valuation does not work in reverse as 1 stETH is only redeemable for 1 ETH once the Ethereum Merge (i.e., ETH2) has occurred. This means that a stETH token trades at a discount to ETH as the underlying asset is locked from the holder, although largely paired at a near 1:1 value as shown in the below chart.

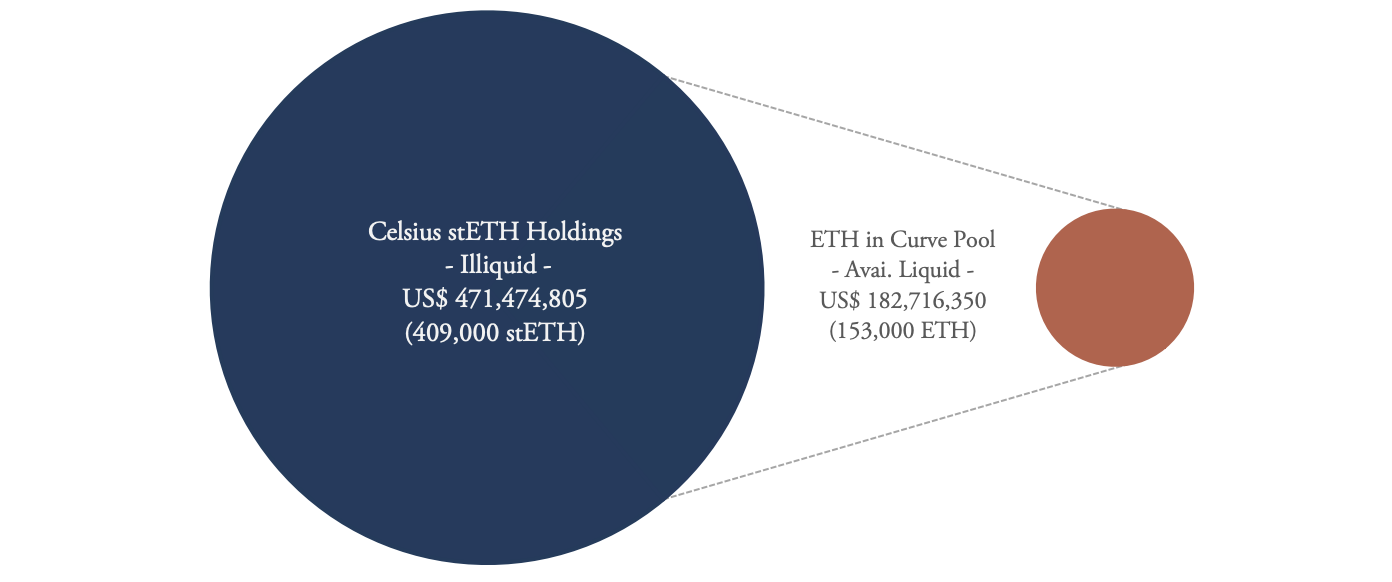

Celsius had allocated nearly half their client’s ETH deposits to stETH, approximately a US$500m exposure to generate yields of up to 6% on client ETH deposits. stETH is traded primarily on Curve, the largest decentralised exchange with daily liquidity capability of approx. US$30m only. This indicated that Celsius would not be able to settle all immediately callable deposit accounts, as its stETH holdings were 16.67 times greater than the available daily liquidity in Curve.

Celsius’ Insolvency Concerns

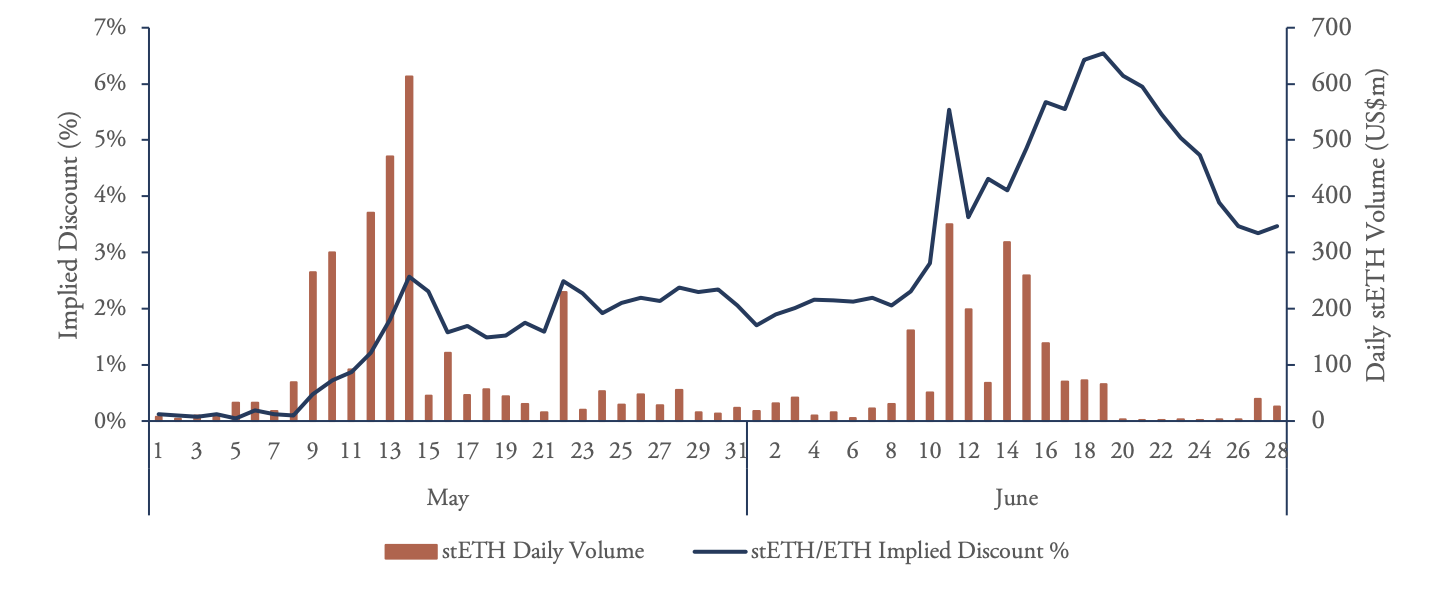

The recent market volatility resulted in the price of stETH deviating from the price of ETH and causing stETH to trade at a significant discount to the collateralised asset ETH, as depicted in the chart below. As Celsius’ stETH holdings devalued heavily and the instances of withdrawal requests increased at an unprecedented rate, Celsius increasingly had to sell more units of stETH to satisfy one withdrawal of ETH, whilst the available liquidity for stETH sales remained incapable of meeting Celsius’ rising selling pressure.

As the issue compounded, Celsius could not sell stETH on the open market and buy ETH, given that over supplying the market would ultimately outstrip demand and cause the price of the collateralised asset stETH to fall further and render Celsius insolvent. As indicated by the chart below, Curve was the exchange that had the most liquidity for stETH yet was not capable of meeting the selling demand, only holding 153,000 ETH available to be traded for stETH, representing roughly 38% of Celsius’ total liquidity requirement.

As a result, Celsius could not attempt to sell its entire holdings in this method, as the market supply of stETH would greatly increase thereby devaluing the asset. Additionally, likely could not Celsius sell over-the-counter (OTC) or off market in order to mask the inflationary impact of an on-market sale, given the illiquid nature of the stETH market.Lastly, no government sought to intervene by purchasing the stETH holdings to settle Celsius’ accounts. This form of intervention is more common in traditional finance, where a reserve bank purchases back government bonds to ease pressures on regulated traditional banks.

However Celsius can use the stETH as collateral to acquire ETH, thereby fulfilling withdrawals and meeting short-term liquidity needs. Celsius currently has a 9-figure stablecoin loan against its stETH holdings on decentralised finance(DeFi) protocol AAVE for liquidity. Additionally, Celsius has taken another 9-figure loan with MakerDAO against theirWrapped Bitcoin (WBTC), a 1:1 derivative Bitcoin unit traded on the Ethereum Network (ERC-20). The true dollar value of the crypto collateralised positions held by Celsius is not known.

Celsius is risking default/insolvency based on the value of the stETH price fluctuations and the high-risk remedial loan positions that it has subsequently taken with other DeFi providers, all the while freezing withdrawals and leaving investors without liquidity.

DeFi/CeFi at Risk

Despite the natural protections of a decentralised ecosystem, the contagion effect has heavily impacted DeFi and CeFi sector participants following high market volatility, macroeconomic headwinds, and shrinking liquidity.

Three Arrows Capital (3AC), a crypto hedge fund established in 2012, is also facing insolvency. At one point, the fund had over US$10b of assets under management, however 3AC had US$500m invested in LUNA currently returning a100% loss with no signs of recovery. Investors in 3AC were forced to liquidate their positions, such as Voyager issued a notice of default to 3AC over US$675m worth of loan obligations. Grayscale Bitcoin (GBTC) is suffering losses due to long positions held on stETH, resulting in many bad loans made across the DeFi sector which are struggling to be called back.

While there is no designated lender of last resort and no GFC-style government bailout incoming, Sam Bankman-Freid of FTX is positioning to bail out companies such as Voyager and BlockFi through aggressive lending.

from Caleb & Brown Cryptocurrency Brokerage.

_.webp?u=https%3A%2F%2Fimages.ctfassets.net%2F4ua9vnmkuhzj%2F2lvgRSrJbfJtXL51ennc1m%2F357dc72a9a6e01352e24cdb0873f77e3%2FC_B012_Blog_Tile_What_Is_Tether_Gold__XAUT__.png&a=w%3D3840%26h%3D2160%26fm%3Dwebp%26q%3D80&cd=2026-02-18T01%3A48%3A36.911Z)